3rd Quarter 2016 Canadian Economic Update – Your Dollars & Sense

QUARTERLY HIGHLIGHTS Q3 – JULY 2016 – VERICO’s Economic Consultant, Michael Campbell helps us to understand the impact of the Brexit vote to leave the EU on our markets, what’s going on with mortgage rates, and who is demanding “government do something about high prices in Vancouver”. – A VERICO Exclusive.

INTERNATIONAL SCENE

Brexit is important because it is a part of a much bigger story. The key to know is that the Brexit vote and demise of the European Union is driven by economic and financial events, not politics. The politics that media is so fond of focusing on is a by-product of the dismal economic and financial performance. If the European’s economy and job creation were booming there would be far less dissatisfaction with the EU – and no Brexit vote or the surge in anti-EU parties.

The gross mishandling of the refugee crisis also exacerbates the dissatisfaction with the EU establishment. Of course there are numerous other complaints but none would resonate with the same level of passion if the economy was strong.

WHAT DOES THIS MEAN?

The biggest immediate impact of the UK vote and the rise of anti-EU parties will be on the currency markets because the euro will no longer be seen as an alternative to the US dollar. The European Union’s uncertain future assures that money will flow out of the euro for years to come and the first choice will be the US dollar.

Every currency including the loonie will fall versus the greenback but don’t worry because the Canadian dollar will be stronger versus the euro and the pound. I’ve been predicting for years that money flowing out of Europe and into the US will fuel a major bull market in quality American stocks.

Another important consequence of Brexit is that the uncertainty in Europe is a negative for global economic growth, which is already slow. That in turn will diminish demand for oil, which will bring prices lower unless there’s a major supply disruption.

Translation – the recovery in Alberta will be slow, which will be negative for employment growth and the real estate recovery in that province.

INTEREST RATES WILL STAY LOW

INTEREST RATES WILL STAY LOW

The Federal Reserve is dying to raise rates but the economic performance both in the US and globally doesn’t warrant it. And now the uncertainty in the UK and European Union will force them to continue to play the waiting game.

In Canada there is absolutely no economic pressure to raise rates. Stephen Poloz must be lying awake at night dreaming of the days when economic growth will be strong enough to be called mediocre. I say dreaming because outside of BC – there’s not many happy places.

And that is not going to change as long as the three levels of government combine to take increasing amount of money out of people’s wallets. One month its increased property taxes, the next a jump in payroll taxes and higher fees for government services the month after that Throw on an increasingly expensive regulatory burden and the recipe for slow motion growth is in place.

The bottom line is that there are no factors that merit pushing interest rates higher in Canada.

SHOCKING SURVEY RESULTS:

100% – the percentage of first time home buyers who would like to see lower home prices

0% – the percentage of homeowners willing to sell their homes for less in order to increase affordability

RESIDENTIAL REAL ESTATE

RESIDENTIAL REAL ESTATE

So much talk about affordability, high prices, foreign owners, speculation, empty houses, and dirty money. Throw in political opportunism and it’s not a recipe for rational discussion, let alone sound policy.

Our public discussion would benefit greatly by making a distinction between affordability and high prices but that would make too much sense. Instead we hear cries of “government has to do something”.

My response is that they already have. Record low interest rates gave helped propel – along with population increases – entry and mid-level homes to record highs. The payments on an average five year $250,000 mortgage in 1995 are the same as the payments on a $450,000 mortgage today.

The assorted development costs in Vancouver for an 800 square foot condo in a new concrete building add about $76,000 to the cost.

Throw in property purchase taxes and I suggest that government has already “done” enough.

The problem for government is that there is no tooth fairy and there is no magic policy bullet. Think about the superficiality of the political talk.

“End Speculation” – but what’s the definition? “Increase density” – but what about the change to the character of the neighbourhood? Penalize foreign owners – but do you support the same measures for Canadians who own real estate in the US?

The point is there are no easy fixes as long as the population growth far outstrips supply. Literally thousands of people arrive in the lower mainland every month needing housing. Supply hasn’t kept up and there is no chance it will when it comes to single detached homes while condo developments haven’t been able to keep pace.

The supply / demand imbalance, along with high prices have sent buyers from Vancouver to Victoria, Nanaimo and Kelowna – with a vengeance. Those markets are enjoying a booming 2016 with significant price appreciation due to demand that the supply can’t satisfy.

Can the municipal, provincial, and federal governments do anything that will make a significant difference? I don’t see it. If government got rid of suspected dirty money, absentee foreign owners, taxed empty homes and discouraged speculation it won’t solve the affordability problem and at best slow the rate of price rise at the upper end.

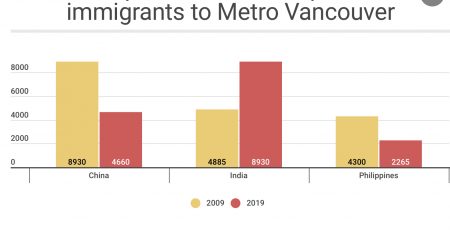

It’s interesting to note that the media coverage of the outcry over high prices has been one sided. After all, there is not a homeowner in the province who is unhappy with the price gains. And there’s not one who would be willing to sell at 2009 prices in order to help with affordability.

CAUTION

CAUTION

The danger for the lower and mid-level end of the market remains a significant move up in interest rates. For the higher end changes in capital flows out of China and other countries would have a major impact on volume. The $5 million plus homes cannot be supported by the local demand.

The sharp increase in prices at the upper end is slowing, which will reduce volumes but a significant price drop will only occur if the pullback of foreign buyers was the result of a credit crunch.

When it comes to the impact of China’s internal debt problems there is a fine line as to whether it’s a positive or negative for our market. So far, problems in China have encouraged money to flow out of the country in search of safety but that could turn quickly if there is a credit crisis.

5 VERY SIGNIFICANT NUMBERS YOU SHOULD KNOW

17,000 – Net in-migration from other provinces to BC in 2015. (25,000 est. for 2016)

144,000 – The number of net new jobs created in Canada last year

110,000 – The number of new jobs creatd in BC led by construction

$1.3 Trillion – The amount of money that left Russia to invest in other countries last year

$1.2 Trillion – The amount of money that left China in the last year (Hello US, Canada, and Australia)