How does the Bank of Canada’s interest rate hike affect variable rate mortgages?

[Globe and Mail – July 13, 2022]

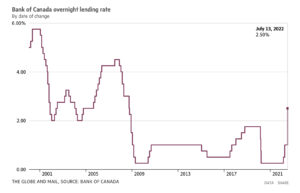

The Bank of Canada increased its benchmark rate by a whole percentage point on Wednesday, the most aggressive rate hike since 1998 and an even bigger jump than investors and Bay Street economists were expecting. This is the fourth consecutive interest rate hike since March, as central banks around the world attempt to curb runaway inflation and slow the pace of consumer price growth. The Bank of Canada’s policy rate now sits at 2.5 per cent.

Rapidly rising borrowing costs are already putting pressure on certain segments of the Canadian economy, most noticeably the housing market, which has seen declining prices and a slowdown in recent months. For homebuyers, being able to afford mortgage payments is increasingly becoming an additional hurdle to purchasing property.

The impact that interest rate hikes have on homeowners and homebuyers depends on whether they have a fixed or variable rate mortgage. Those with variable rate mortgages that adjust with the prime rate are more exposed to benchmark rate increases and may be concerned with current trends.

With that in mind, here’s what you need to know about how mortgage rates will be impacted by rising interest rates.

What’s a variable rate mortgage?

A variable mortgage rate fluctuates based on the so-called prime rate, a benchmark lenders usually adjust based on movements in the Bank of Canada’s trendsetting overnight rate.

Lower rates on variable-rate mortgages have attracted homebuyers in recent years. As of April, they accounted for 37 per cent of new insured mortgages, according to the latest data from Statistics Canada and the Bank of Canada, compared to just 5 per cent of mortgages in January, 2020.

What’s a fixed rate mortgage?

A fixed interest rate mortgage typically locks in payments for a set term of two to five years. Fixed rates are often higher than variable rates, but offer peace of mind to homeowners that their mortgage payments will be consistent for the years to come.

What is Canada’s prime rate and how will it affect variable rate mortgages?

The Bank of Canada’s increase was for the policy rate, which operates as a target for the daily overnight rate, which in turn is the basis of variable rate mortgages.

The prime rate is the annual interest rate Canada’s major banks and financial institutions use to set interest rates for variable loans and lines of credit, including variable-rate mortgages. As policy rates go up, prime rates go up, which ultimately raises the rate of interest that you pay on your loan. The prime rate in Canada is currently 3.70 per cent.

Will mortgage payments go up because of the Bank of Canada rate increase?

When interest rates rise, homeowners pay more in interest. However, not everyone will see their monthly payments increase when rates climb.

Some variable-rate mortgages keep payments steady – up to a certain threshold, known as the trigger rate – even as the interest rate moves up. Instead, these borrowers pay more interest and less on the principal monthly, and see their amortization period extended, meaning it will take longer to pay off the mortgage.

But if interest rates continue to rise, interest payments could increase when the trigger rate is surpassed.

What’s a trigger rate?

The “trigger rate” is the interest rate level that, when surpassed, causes a mortgage holder’s monthly payments to change. The trigger rate has been largely ignored for decades, because the last time Canadians had to deal with fast-rising rates was the late 1970s.

Now that interest rates are rising, borrowers are moving closer to their trigger rate – a level at which their regular monthly payments will not be enough to cover the interest for the period.

The exact triggering rate is different for every mortgage holder and depends on the size of their loan, the amount of their monthly payment, the interest rate of the mortgage and length of the amortization period.

Can I convert my variable rate mortgage to a fixed rate?

It is not possible to switch from a fixed to variable rate without breaking the mortgage contract (which results in a penalty).

However, it is possible to go the other way. You can lock a variable rate mortgage into a fixed rate one at any time, without breaking the mortgage contract – and if you break the contract with a variable rate, the penalty is often much lower.

Should I convert my variable rate mortgage to fixed?

Variable-rate mortgages tend to be cheaper than fixed-rate mortgages, in which the borrower pays the same interest rate for the term of the loan. The rate on the most common fixed term (five years) increased to 4.41 per cent in early June from 2.21 per cent a year earlier, according to Bank of Canada data. Meanwhile, the variable rate mortgage rose to 2.72 per cent from 1.63 per cent over the same period. Further Bank of Canada interest rate hikes will be reflected in variable rate mortgages and new fixed-rate mortgages.

Switching from a variable to a fixed-rate mortgage typically requires you to pay a penalty equal to three months’ worth of interest, depending on the lender. However, you may not be able to lock in at the most competitive fixed rate available, and the terms of your mortgage may stay the same. That means whatever fixed rate you are converting to might only be valid for the remainder of time on your current term, and you will be forced to renegotiate that rate once your mortgage is up for renewal.

That being said, the risk of locking in, especially with a five-year term, is you may get stuck paying a lot of interest if trends change. Staying with a variable rate means you’ll ride lower rates once inflation has peaked. If Canada heads into a recession, interest rates could fall quickly. It is also costly to switch from a fixed-rate mortgage back to a variable one, as that comes with a higher penalty.

The biggest factors to consider when making the switch are your risk tolerance and the size of your mortgage. In general, locking in is less appealing when variable rates are significantly lower than fixed ones; however, it’s important to consider your ability to keep up with your variable mortgage if rates continue to rise. Also, interest rate hikes have a lower impact on homeowners with variable-rate mortgages that are small or significantly paid off.